Congratulations All who invested in Likhitha Infrastructure our Feb 2021 Multibagger. This post is just for Reference Purpose & Not any Action to Buy now. If you are Interested in New Multibaggers you can Avail Subscription Here!

SUBSCRIBE THE BEST PERFORMING DISCOUNTED STOCK ADVISORY SERVICE OF INDIA

| NSE Code | LIKHITHA.NS |

| BSE Code | 543240 |

| Group | B |

| CMP | 211.00 |

| Max Buy Price | 250.00 |

| Capitalization | 400 CR |

| Company URL | http://www.likhitha.co.in/ |

| Date | Feb 2021 | Premium Multibagger |

INTRODUCTION

Likhitha Infrastructure established in the year 1998 in the business of Pipeline Laying providing comprehensive erection, testing and commissioning of Oil & Gas Pipelines, City Gas Distribution Projects and Operation and Maintenance (O & M) Services.

The company is promoted by Mr. Gaddipati Srinivasa Rao, a technocrat having vast technical experience of over 3 decades in the field of laying of Cross-Country Pipeline of hydrocarbons and City Gas Distribution Projects.

The company is having operations in 75+ countries and growing with 30% CAGR annually. It is also predicted to benefit from the Infrastructure Growth of India especially highlighted in the Budget 2021 where 5.5 Lakh Crores allocated on Highways, Gas Infrastructure, Distribution systems.

The company recently came with IPO during Sep 2020. The price moved up around 100% from the IPO price which shows the mis-priced opportunity on a growth company.

GROWTH FACTORS

Services: The services provided by company include three principal business lines:

- Cross Country Pipelines and associated facilities

- City Gas Distribution including CNG Stations

- Operation & Maintenance of CNG/PNG services.

Experience & Exposure 20+ year’s experience in diversified operations in states of Karnataka, Delhi, West Bengal, Gujarat, Andhra Pradesh, Telangana, Kerala, Madhya Pradesh, Jharkhand, Bihar, Chandigarh, Haryana, Orissa and Uttar Pradesh. Executed the first Trans-National Hydrocarbon (Multi-product) Pipeline Project between India and Nepal

Moat ISO 9001:2015 by International Certification Services Pvt Ltd for specialization in the field of Design, Construction of Cross-country pipelines, City Gas Pipelines and Civil Constructions.

Client Base Working on PSU projects in India & Have presence in 75+ countries. No impact on growth during the COVID times too.

Opportunity Energy Consumption of India to grow with 20% allocation in gas due to additional RLNG terminals and transnational pipelines are expected to come in 2025-2030 timeline. Commissioning of LNG Terminals in West Coast, Government Initiatives, Transportation of Gas throughout India would materialize the Cheapness Advantage of Gas compared to Diesel & Petrol – all these would give the company 5X growth in revenue & 10X growth in prices due to the MF investing & PE resizing.

Revenue Growth: The company is witnessing CAGR of 30% growth on an average yearly basis. The COVID lock-downs impacted the work-in-progress of the company due to Labor availability otherwise the Order Book processing are not without a gap.

Budget Acceleration With the accelerated budget of India 2021 with 5.5 Lakh Crore allocation in Infrastructure & Introduction of Infrastructure Financing facilities by Government – the company will witness even more growth.

Expansion Company is expanding the Gas Pipeline Laying Capacity to 300 Kilometers per year to accommodate the India Gas Pipeline expansion of 100% to 35000 kilometers in 5 years.

Intrinsic Value Discount The company is trading at 70% Intrinsic Value based on the Average EPS Growth of the past 3 years.

Pricing The company recently came with IPO during Sep 2020. The price moved up around 100% from the IPO price which shows the mis-priced opportunity on a growth company.

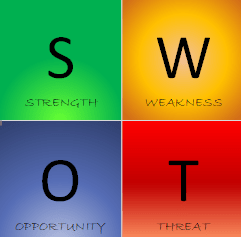

SWOT Analysis

SWOT (Strength-Weakness-Opportunity-Threat) Analysis:

| STRENGTH Operational Excellence PSU Support Global Clients Expansion Plans No Debt | WEAKNESS Rising Raw Material Costs Availability of Big Players |

| OPPPORTUNITY India Expansion Global Expansion Capital Moat prevent other players | THREAT Delay in Govt Payments |

BCG Matrix

BCG (Boston Consulting Group) Matrix is Dog since the Sector has low growth potential & the company is having a low share currently.

P&L

In the past the company witnessed 30% above compounded growth in Revenue, Net Profit & EPS. The current year results including QR is also growing at 50% rate.

The past year growth in revenue & profits.

CHECKLIST

Following are the Core Checklist to ensure Value & Growth Parameters.

| Parameter | Description | Legend |

| Revenue Growth | Yes |  |

| Profit Growth | Yes | |

| Profit Margin | Good | |

| EPS Growth | Good | |

| Trailing Growth | Yes | |

| PE Ratio | 21 |  |

| PB Ratio | 5 | |

| PEG Ratio | 0.5 | |

| DE Ratio | 0.0 | |

| Current Ratio | 4 | |

| Quick Ratio | 3 | |

| ROE | 33% | |

| ROCE | 44% | |

| Reserves | Increasing | |

| Cash Flow | Positive | |

| Paying Tax | Yes | |

| Paying Dividends | No | |

| Power of Brand | Moderate | |

| Future Sector Growth | Yes | |

| Expected Company Growth Rate | 20% | |

| Expansion Plans | Yes | |

| Promoter Holdings | 74%, Increasing | |

| Corporate Governance | Yes | |

| Fraud Reported | No | |

| Celebrity Investors | Yes, few exists | |

| Trading at Discount | No | |

| N-Point Checklist | 50 point | |

| Risk Category | Moderate-Risk | |

| Returns Category | High-Returns | |

| Advisor Invested | Planning to Invest | |

RISKS

Following are the Risks associated with the investment:

- Rising Material Cost would impact the Profit of the company

- COVID Lock-down Extension would affect the Work deliverables

- Government Fund Allocation delays in Infrastructure are a Threat

- Large Players like L&T, GMR, Adani are Threat to Contract Assignments

SUMMARY

Given the Facts & Analysis we recommend this company as a Multibagger in the order of 500% 5-bagger plus returns for a 5-year holding period.

BUYING STRATEGY

You can Invest 50-70% in current price & accumulate remaining as monthly installments in next 6 months. Any crash in price is an Opportunity.

Current Price compared to 52 week high may be high but the Valuation based on PE, PB & Intrinsic Value Discount shows Low. Hence any corrections are opportunity to buy till the Portfolio Limit of stock reached.

PORTFOLIO ALLOCATION

The Investor is required to undergo efficient portfolio management. Here is the link on same.

DISCLOSURES

Futurecaps is the website registered as a Research Analyst with SEBI (INH2OOOO6956) offering investment advisory services to clients as well as prospects. The Research Analyst (not a corporate body) for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to the recommendations or views expressed in this report. Other disclosures by Research Analyst with reference to the subject company(s) covered in this report-:

Whether Research Analyst does have any financial interest in the subject company: (YES, holding shares)

Whether Research Analyst relatives have financial interest in the subject company: (NO)

Research Analyst or his/her relative’s does have any material conflict of interest in the subject company: (NO)

Research Analyst or his/her relatives have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of Research Report: (NO)

Research Analyst has served as officer, director or employee of the subject company: (NO)

This report is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. This report is created from Public Source of Information available through Internet from Company website & Other websites & the Research Analyst does not guarantee the Validation of Content in this report. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is for the general information for the Subscribers of Futurecaps. While reasonable care has been taken in the preparation of this report, it does not purport to be a complete description of the securities, markets or developments referred to herein, and we do not warrant its accuracy or completeness. Futurecaps Research Analyst or representatives do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report.