Most people will NOT agree with this statement – but In Investing Terms House is NOT An Asset!

Robert Kiyosaki the International Financial Coach repeats that House is NOT an Asset!

Let us try to understand why he said so.. [this article involves calculations – but will save you crores if you learn it]

A House can take away Rs. 10 Crore of Yours!

If you are in the Verge of buying a House – Spend few money on learning which will give you back Crores!

Robert Kiyosaki Definitions

Robert Kiyosaki used the following Definitions:

Investment Benchmark 10%

In India the base Investment Benchmark is 10% which is the Returns on Long-Term Fixed Deposits like Corporate FD, Bonds etc. These are NO Activity NO Risk kind of returns.

So if you choose any Investment it should be having Higher Return than the Benchmark 10%.

Also note that If your Investment requires more activities & monitoring then the corresponding returns also should increase.

Rule of Thumb Any Investment which involves Activities & Risks should be having more Returns than the above Benchmark 10%!

WHY HOUSE IS NOT AN ASSET IN INDIA?

In India the Returns on House as an Investment is very low of 5% Only!

- Appreciation 5%

- land appreciation 8%

- building depreciation -3%

- total 5%

- Rental Savings 2%

- Maintenance & Taxes -2%

So approximately you will get Only 5% Returns on a House!

- If you compare with Long Term Corporate Fixed Deposits of 10% – You are at Loss

- If you compare with High Returns in Stocks/Mutual Funds like 30% – You are Loosing a Fortune!

Smart Investor does what?

A smart investor is having access to 30% Return investment opportunities like stocks, mutual funds etc. as he invested time learning them. Stocks & Mutual Funds associates Higher Risks & It requires Training – but worth the 30% ROI they provide in Long Term & Compounded.

So instead of buying a home the Smart Investor prefer to Go for Rent in a Similar House and Invest the Capital into 2:

- Start a Long Term FD of 30 Lakhs which generates 10% interest to pay the rent and rental increases

- Put the remaining 70 Lakhs in high growth investments of 30% more returns

Note: 10% Interest FD is easy – We have also provided 15% yielding FDs to customers

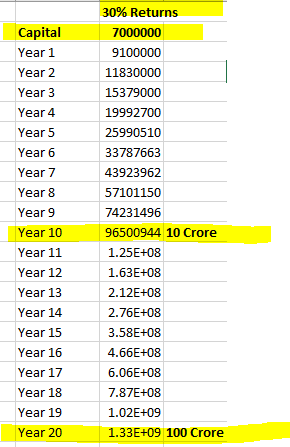

After 10 years there will be:

- Fixed Deposit & Rental is going as it is

- You will see Rs. 10 Crore compounded returns in stocks – 10X the return than the house investment

Now the Smart Investor can sell the Stocks and Buy a Big Mansion House + Put Remaining Money for Cash Flow attaining Financial Freedom too.

After 20 years the assets will be so huge

- Fixed Deposit & Rental is going as it is

- You will see additional Rs. 20 Crore in the stock capital

At this point the Smart Investor would have generated Wealth & Income for Generations. REAL Financial Freedom!

If you waste 1 Crore today – You are actually wasting Rs. 10-100 Crore in future!

This is the reason Smart Investor wisely goes for Rent & Allow Money to Grow!

While the Poor Amateur Guy will go with Buying the House & Loose the Financial Freedom!

Note: If you add Loan on House – then the ROI will become worse as you are paying 8% Interest for a 5% Returns!

Then who is buying the houses?

Mostly, the middle class are buying the houses. They are happy with own house as it is an emotion. Plus, they think they are saving rent, but in net effect they are only gaining low 5% returns. The middle class are not trained financially – they don’t spend money on learning – hence they loose crores!

Most of the middle class takes a 150% loan on top of the house thereby becoming slaves of banks for their entire life.

Builders rob the middle class with high priced properties.

Banks rob the middle class with high interest loans.

Middle class guys are just Victims!

Government & Banks nurtured a culture of OWN HOME AS A DREAM so that people would spend mindless money on dreams. Then the middle-class owner will get locked themselves for Owning the Dream while the economy gets their work blades cutting, banks are happy with interest & government enjoy taxes.

So What do the Rich Class Do?

The Top Riches will be Renting Houses rather than Owning as Renting is Profitable in India!

Riches only Buy a House only when they are Financially Free or Huge Wealth is amassed. House will be < 10% of their Net Worth. They make remaining 90% money work for them.

While Middle Class take 150% Loan on their Net Worth and Works for Money whole life!

Example: Mukesh Ambani bought Antilla while it was less than 10% of his net worth & his remaining 90% Net Worth is working for him.

All the top riches like Bill Gates, Warren Buffett use this 10% Formula for their house, cars & jets which are Liabilities / Low-Return Assets. Their remaining 90% money always works for them.

The Big Problem

The bigger problem on owning a house it that you will loose another 10 Crore too. How?

The owned house will make you Stagnant at one location, you cannot move out to other state or country for better job opportunities. Hence you will loose another 10 Crore from Job Opportunity Loss too.

The Solution

So if you are Not in a Hurry to Buy a House, then you may Postpone the Buying for few years & let the capital grow.

- If you are in Age 30-40 range and wanted to Grow your Career Abroad, then you can Postpone buying the house & after 7-10 years you will have Immense Wealth and Cash Flow to be Financially Free & Boast with a Mansion & BMW too.

BE FINANCIALLY SMART & LIVE LIKE A KING!

Summary

- House is NOT AN ASSET as it a low return investment

- 90% of Home Loan Buyers have locked their Life for Financial Slavery

- Rich Class do not consider House as Investment – But as Luxury EnjoyabeToys like BMW & Mercedes cars which depreciates

- Rich Class chooses 30% ROI Investment Vehicles – They put 90% Net Worth on these and thus Nullify above Depreciation

- Don’t be an Amateur Investor – Be a Smart Investor!

- Learn other 7 Smart Investor Strategies in our MASTER MIND TRAINING

- How to Evaluate Real Estate, Stocks & Any Investments?

- How to buy your Luxury House free of cost?

- How to Handle your Net Worth?

- How to Achieve Financial Freedom in 5 Years?

- How to Gain 30% Returns from Real Estate using Rich Class Strategy?

- How to Gain 30% Returns from Stock Market using Rich Class Strategy?

- 1 Hour Consultation with Advisor

Remember another Middle Class Bad Habit – They won’t Invest money in Learning & Learn from Failures at Higher Cost!

Testimonials

- Raj Chennai I was having a 1 Crore Ancestor Property yielding only 1% Rent along with Maintenance & Tenant Issues. I was not planning to live there for next 5 years – Based on your Secret Strategy I converted that to a 20% ROI Property. Now in few years I can buy a new house free of cost with the Income & My Extra Job Savings while having Financial Freedom too – Thanks for the Great Idea!

MASTER MIND TRAINING Acquire the Skills of a Smart Investor – Stock Market, Real Estate, Valuation in Just 3 Months! Rs. 9999 Only!

FUTURECAPS | BEST VALUE ADVISOR INDIA